Researchers

Margot Mollat Date of publication

25 November 2025

Download

Document

Opening Up Offshore Secrecy

(1.61 MB)

Introduction

Since the Panama Paper leaks in 2016, offshore finance has come under mounting international scrutiny. The revelations exposed how shell companies, trusts and complex corporate structures are used to divert public funds, launder money, and avoid paying taxes. The UK, and its network of Overseas Territories and Crown Dependencies, are at the centre of this global shadow system, which allows billions of pounds to be siphoned away each year.

Over the past decade, there has been growing recognition that the secrecy offered by these offshore financial centres is what makes them attractive to nefarious actors seeking to hide their identities and launder the proceeds of crime. This has serious implications for the UK’s economic integrity, national security and global standing, as well as devastating effects throughout the world.

Our previous research found that opaque vehicles registered in the UK’s Overseas Territories have been used in more than 273 cases of large-scale corruption and money laundering, amounting to USD$327 billion (£250 billion) in funds diverted through rigged procurement, bribery, embezzlement, and the unlawful acquisition of state assets across 79 countries.

Recognising that corporate secrecy has played a key role, successive UK governments have sought to work with offshore financial centres to crack down on this issue and create registers naming the ultimate owners of companies registered there – known as beneficial ownership registers. Following an amendment introduced in the Sanctions and Anti-Money Laundering Act (2018), the UK Overseas Territories committed to establishing public registers.

However, momentum was disrupted by a 2022 European Court ruling, which found that fully public registers conflicted with privacy rights. Although not binding on these jurisdictions, many of them cited the ruling as they scaled back their stated ambitions for public registers in favour of emerging EU standards’. Set out in the sixth anti-money laundering directive (AMLD6), the EU requires that only those with a ‘legitimate interest’ in beneficial ownership information would have access to it. Certain groups – including journalists, academics, and civil society organisations working to combat money laundering – are presumed to have a legitimate interest and therefore receive open access to the data.

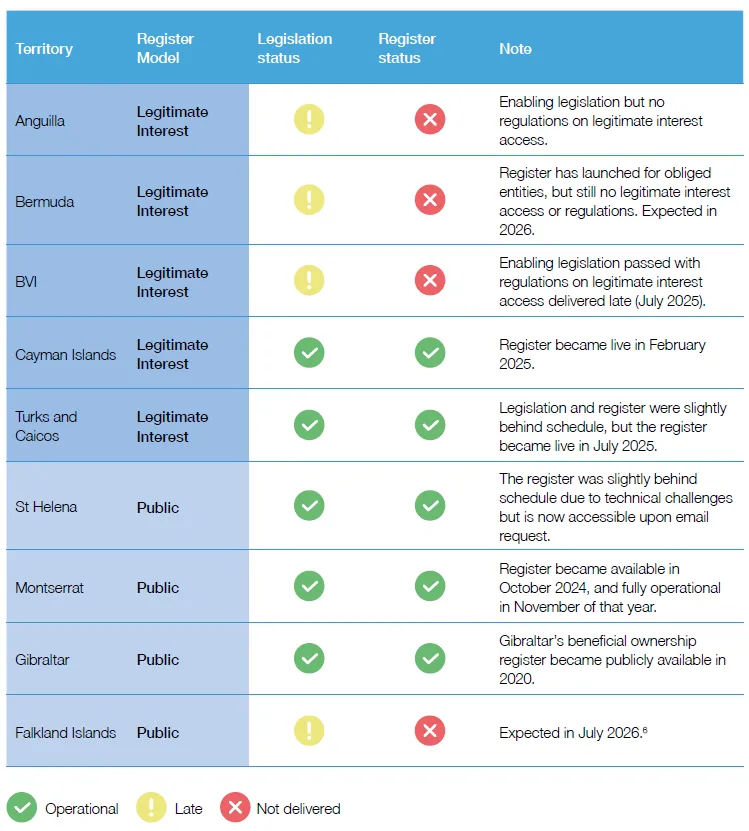

At the November 2024 Joint Ministerial Council in London, Overseas Territories without publicly available registers committed to ‘implement Legitimate Interest Access Registers of Beneficial Ownership (LIARBOs) with the maximum possible degree of access and transparency, whilst containing the necessary safeguards to protect the right to privacy in line with respective constitutions’.

Using the EU model as a reference, as well as other standards in the UK, and Guidelines by the Financial Action Taskforce, Transparency International UK published a blueprint for ending secrecy in British offshore centres. This assessment measures the progress of four Overseas Territories against these guidelines, marking Bermuda, the British Virgin Islands, Cayman and Montserrat against the standards they have agreed to.

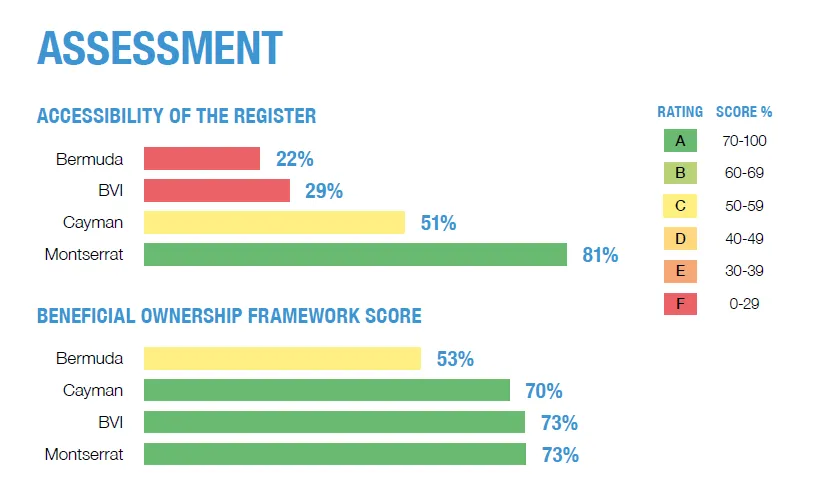

Assessment

Key Findings

- Seven years on, progress is slow. Nearly seven years after the UK Parliament called for public registers of beneficial ownership in the UK’s Overseas Territories, progress remains slow, especially in jurisdictions that present heightened risk for money laundering. Many jurisdictions have missed political commitments, legislative deadlines, and operational milestones, raising concerns about their willingness to deliver meaningful transparency.

- The shift to “legitimate interest” models is more costly, complex and offers much weaker transparency. Several Overseas Territories have opted for EU-style legitimate interest access regimes rather than the straightforward public registers they originally committed to. In practice, these regimes are being developed in a piecemeal and inconsistent way, falling short of the standards set out in AMLD6. This severely limits the ability of journalists, civil society, foreign law enforcement, and others to help combat money laundering.

- Proposed legitimate interest frameworks risk producing incomplete or unusable data. There is a real risk that those who gain access to beneficial ownership data will receive incomplete information still hidden behind trust structures, or that users will be unable to use the data for legitimate purposes. In some cases, access could even alert nefarious actors, giving them a head start to hide assets or take legal action.

- Only a handful of jurisdictions – Gibraltar, Montserrat, and St Helena – have established fully public registers.

Recommendations

To ensure the Overseas Territories deliver on their existing transparency commitments, the UK Government should:

- Press UK Overseas Territories to provide meaningful access to beneficial ownership data in line with international standards, which at a minimum should align with the EU directive and with no further delay.

- Reaffirm commitments to public registers as the ultimate objective. They play a vital role in promoting economic growth, safeguarding financial integrity and protecting the UK’s global reputation as a safe and sustainable business environment.

- If any Overseas Territory continues to defy the will of the UK Parliament, the Government should be prepared to escalate its response. All legal and constitutional options should be on the table to ensure these commitments are delivered in full and without further delay.

Progress Update

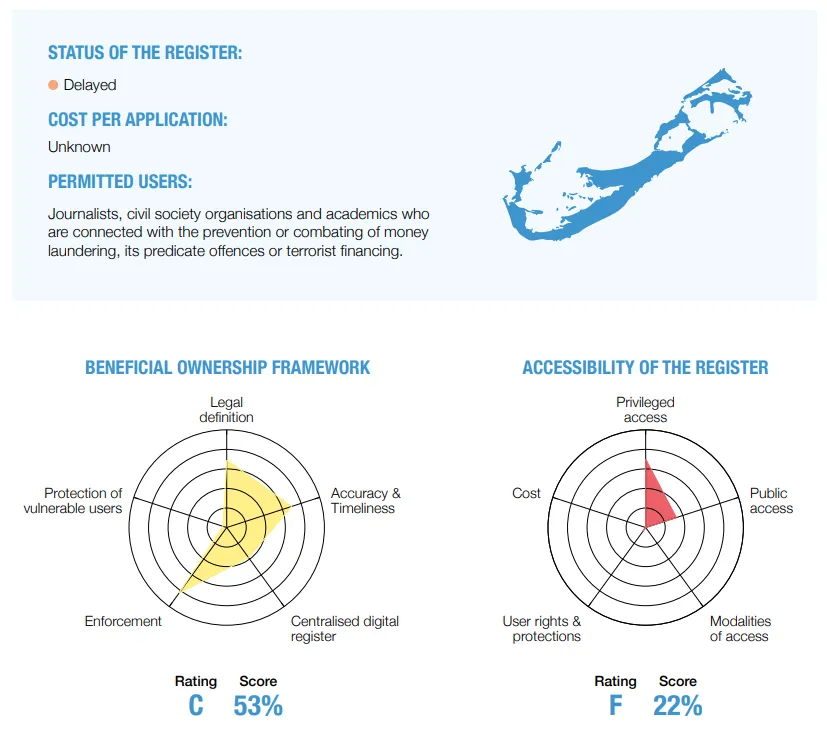

Bermuda

Background

With over 150 islands and islets across the North Atlantic Ocean, Bermuda is the oldest self-governing UK Overseas Territories and a major financial centre.

Bermuda has long maintained a central register of beneficial ownership, which is now managed by the Registrar of Companies, and applicable to a broader range of legal entities.

Risks and vulnerabilities

Key Risks

Money laundering risks linked to foreign predicate offences and the cross-border transfer of funds. The main predicate offences include international tax crimes, corruption, fraud, drug trafficking as well as market manipulation and insider trading.

Vulnerabilities

Though well regulated, the reinsurance sector is inherently risky due to high volumes of large and complex transactions.

FATAF Status

Its 2020 review found that Bermuda was compliant or largely compliant with 39 of its 40 recommendations.

Key strengths

- Beneficial ownership definition largely follows international guidelines.

- Beneficial ownership reporting obligations apply to companies, their owners, and trust and company service providers, with timely deadlines for reporting, and potentially substantial financial penalties for non-compliance.

- Modalities of access: Policy approach suggests that Bermuda will presume that journalists, academics and civil society organisations have a legitimate interest in beneficial ownership information, which is broadly similar to the EU, although it is unclear whether these organisations will have open and repeated access to data.

- Register design: The register follows the Open Ownership data standard and is designed to quickly map relationships between beneficial owners and companies, even in complex structures.

Key weaknesses

- No legislation providing legitimate interest access yet, with relevant laws expected in 2026 – way past their promised delivery date. This has significantly weakened Bermuda’s overall score.

- Unlikely to disclose parties to trusts controlling companies, providing a crucial transparency loophole and undermining the effectiveness of the disclosure regime.

- Lack of clarity over the process for assessing and awarding access to beneficial ownership data.

- No clear intent to protect the identity of legitimate interest users, with a lack of clarity around tipping-off provisions and restrictions on the use of data.

Case Studies

Glencore Paradise Papers Revelations

The Paradise Papers investigation led by the International Consortium of Investigative Journalists (ICIJ) revealed how FTSE 100 company Glencore used its Bermuda operations and offshore structures to facilitate questionable deals in the Democratic Republic of Congo (DRC).

In response to the ICIJ’s allegations, Glencore said that the price for the mining licenses was agreed to before Gertler entered the negotiations and that its loan to the company controlled by Gertler was “made on commercial terms” with standard provisions in place.

Alisher Usmanov

Alisher Usmanov, an Oligarch sanctioned by the UK in 2022 due to his close links to the Kremlin, is known to have used companies based in Bermuda as part of complex ownership structures to hold assets around the world.

How Bermuda can deliver on its transparency commitments

- Promptly introduce access for legitimate interest users, aligning with our blueprint for legitimate access (based on EU requirements). This should grant journalists, civil society, academics, law enforcement and other legitimate users repeated, open, free and meaningful access without requiring individual applications for each entity.

- Protect users acting in the public interest by introducing strong legal safeguards to ensure those accessing the register can use its data to advance a legitimate purpose.

- Enable legitimate interest users to access full beneficial ownership data, including information about parties to trusts controlling companies.

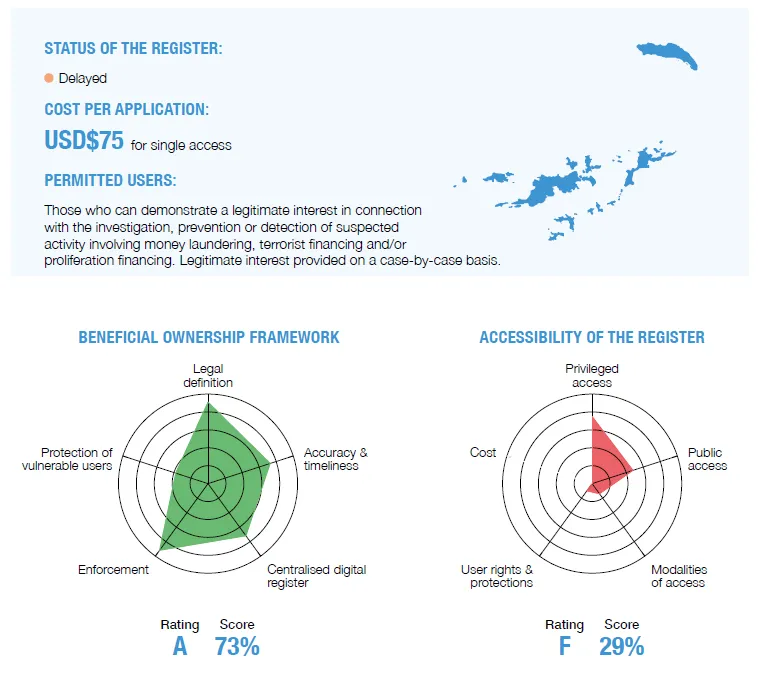

British Virgin Islands (BVI)

Background

An archipelago of more than 50 islands, the British Virgin Islands (BVI) is home to fewer than 40,000 people. While tourism remains a key economic pillar, the jurisdiction is know for its corporate and financial services: trusts, company incorporation and the administration of legal entities. According to its latest estimates, the BVI is home to over 350,000 companies.

Previous Transparency International UK research found that over 90 per cent of companies from the OTs involved in corruption and money laundering in recent decades were incorporated in this jurisdiction, highlighting its outsized role in facilitating illicit finance.

Risks and vulnerabilities

Key risks

High threat from proceeds of crimes generated abroad, including corruption, fraud,

tax evasion and money laundering, especially through Politically Exposed Persons (PEPs). Terrorism financing is also an elevated risk in relation to international transactions.

Vulnerabilities

Trust and corporate services sector serving foreign customers is a major risk in the BVI, especially due to its frequent reliance on professional business introducers for the collection and verification of beneficial ownership information, without verifying their work.

located in the territory, even if evidence of sanctions evasion has emerged.

FATF Rating

In June 2024, FATF added the BVI to its ‘grey list’ for reasons including authorities’ lack of interest in BVI companies’ involvement in money laundering outside of the islands.

Key strengths

- Beneficial ownership definition largely follows international guidelines, with threshold for shareholding as low as 10 per cent.

- Beneficial ownership reporting obligations apply to companies, their owners, and trust and corporate service providers, with potentially substantial financial penalties for non-compliance.

- Privileged access: Data is ‘readily available’ for domestic law enforcement, competent authorities and entities regulated for anti-money laundering purposes, with a duty on those firms to report any discrepancies they identify in the data.

Key weaknesses

- Tipping-off: Proposed approach would provide a slow and time-consuming application process, with tipping-off provisions informing criminals that they are under investigation, and an opportunity for beneficial owners to object to their identity being disclosed.

- No users with ‘presumed’ legitimate interest access, which the EU has given to journalists, NGOs, academics and others connected with tackling money laundering and its predicate offences.

- Unlikely to disclose parties to trusts controlling companies, providing a crucial transparency loophole and undermining the effectiveness of the disclosure regime.

Ambiguous and draconian restrictions on the use of beneficial ownership data.

Case studies

Operation Car Wash

US investigators found executives at Brazilian engineering conglomerate Odebrecht had bribed employees of Brazil’s national oil company using BVI firms Smith & Nash Engineering Company, and Golac Projects and Construction Corporation.

The companies funnelled approximately USD$788 million in bribes across 12 different countries, as part of a scheme dubbed by prosecutors at the time as ‘the largest foreign bribery scheme in history’. Odebrecht pleaded guilty in December 2016 and agreed to pay a penalty of at least USD$3.5 billion.

PrivatBank Theft

In July 2025, the UK’s High Court ruled that Ukrainian oligarchs Ihor Kolomoisky and Hennadiy Boholiubov used a vast network of BVI shell companies, including entities incorporated in the BVI, to steal approximately USD$1.9 billion from PrivatBank, Ukraine’s financial institution.

How the BVI can deliver on its transparency commitments

- Immediately repeal all tipping-off provisions that allow beneficial owners to object to their data being released. They should establish legal safeguards to ensure that beneficial owners are never alerted when their information is accessed or provided with details about an application. It should also ensure those accessing the register can use its data to advance the legitimate purpose under which it was obtained.

- Enable broad, repeated access for key users. Align with our blueprint for legitimate access (based on EU requirements), granting journalists, civil society, academics, law enforcement, and other legitimate users repeated, open access without requiring individual applications for each entity.

Enable legitimate interest users to access full beneficial ownership data, including information about parties to trusts controlling companies.

Cayman Islands

Background

The Cayman Islands, a small archipelago south of Cuba with around 88,000 inhabitants and a GDP per capita of about USD$98,000, is one of the world’s leading offshore financial centres.

In April 2025, Cayman introduced a new beneficial ownership framework, opting to grant access on a legitimate interest basis to those who can demonstrate that the information is required for preventing, detecting, investigating, combating or prosecuting money laundering, related predicate offences, or terrorist financing.

Risks and vulnerabilities

Key risks

Proceeds of crimes generated abroad, including fraud, tax evasion and drug trafficking.

Vulnerabilities

Misuse of legal entities and complex trust arrangements for the investment of laundered funds derived from drug trafficking, tax evasion, corruption and theft.

FATF status

In 2023, FATF removed the Cayman Islands from its ‘grey list’ of jurisdictions subject to increased monitoring for successfully addressing deficiencies in its anti-money laundering framework.

Key strengths

- Definition of beneficial owner almost fully aligns with international guidelines.

- Obligations to report beneficial ownership apply to companies and their owners, as well as trust and corporate service providers, with potentially substantial financial penalties for non-compliance.

- Discrepancy reporting: Explicit requirements on the Registrar and those with access to beneficial ownership records to report and address discrepancies.

Protection of vulnerable individuals: Beneficial owners can only apply to withhold their information from disclosure in limited circumstances and must supply evidence to support their application.

Key weaknesses

- No open and repeated access: Journalists, civil society organisations and academics do not have presumed legitimate interest. Unlike the EU standard, they require applicants to demonstrate a specific legitimate interest in each entity, showing that access would assist in the prevention or detection of money-laundering or its predicate offences. Applications are assessed case-by-case.

- Cumbersome application process: Requests are done through a portal, which requires an international banking transfer, with no option for card payments. The evidentiary threshold for requesting beneficial ownership data is high, with users having to upload documents and a narrative about their investigation. Their policy also lacks clear terms and conditions for users.

- Restricted search functionality: Searches can only be conducted by company name, not by individual beneficial owners or controllers – meaning applicants must already know about the existence of the entity and its relationship to people of interest, which substantially reduces investigatory value.

Unlikely to disclose parties to trusts controlling companies, providing a crucial transparency loophole and undermining the effectiveness of the disclosure regime.

Case studies

1MDB Malaysian Sovereign Wealth Fund Scandal

The 1MDB corruption case represents one of the largest corruption cases in history, with Cayman Islands entities playing a central role by helping disguise the origin, movement, and destination of billions of dollars through complex offshore structures and investment funds.

The US Department of Justice identified numerous Cayman entities used to steal money from the Malaysian Sovereign Wealth Fund, including USD$1 billion sent to PetroSaudi Holdings (Cayman) Ltd

Chen Zhi and Prince Group

In October 2025 a network linked to the Prince Group, a Cambodian criminal organization implicated in large-scale money laundering and investment fraud schemes was sanctioned in both the UK and US.

As part of these sanctions Office for Foreign Assets Control (OFAC) designated four Cayman entities which served as the wealth management arm for the owner of the Prince Group, Chen Zhi.

How Cayman can deliver on its transparency commitments

- Enable broad, repeated access for key users: Align with our blueprint for legitimate access (based on EU requirements), granting journalists, civil society, academics, law enforcement, and other legitimate users repeated open access without requiring individual applications for each entity.

- Enable legitimate interest users to access full beneficial ownership data, including information about parties to trusts controlling companies.

Create a clear and user-friendly access system that allows legitimate users to obtain beneficial ownership information easily and affordably. This should include simple and objective application criteria, renewed access for approved users, transparent decision-making and appeals processes, along with affordable access for those seeking data for noncommercial reasons.

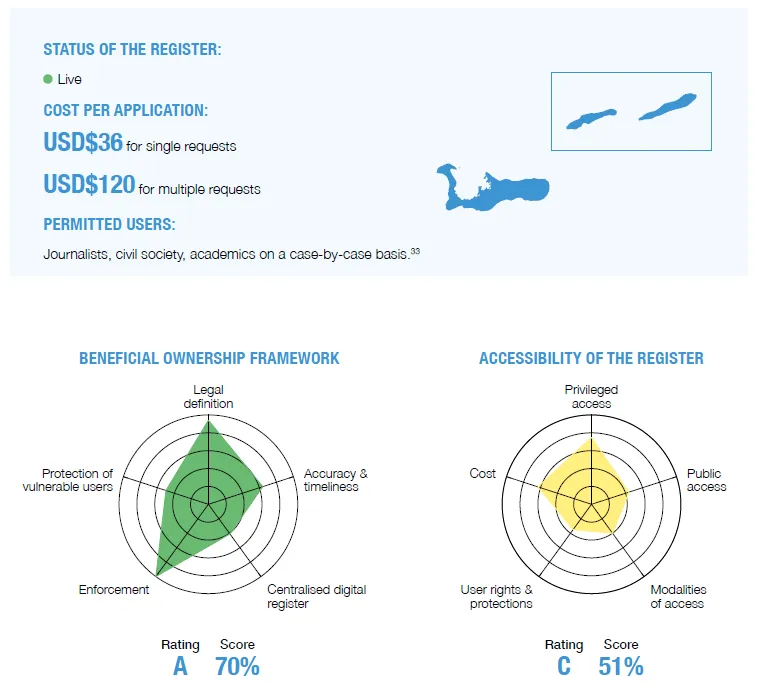

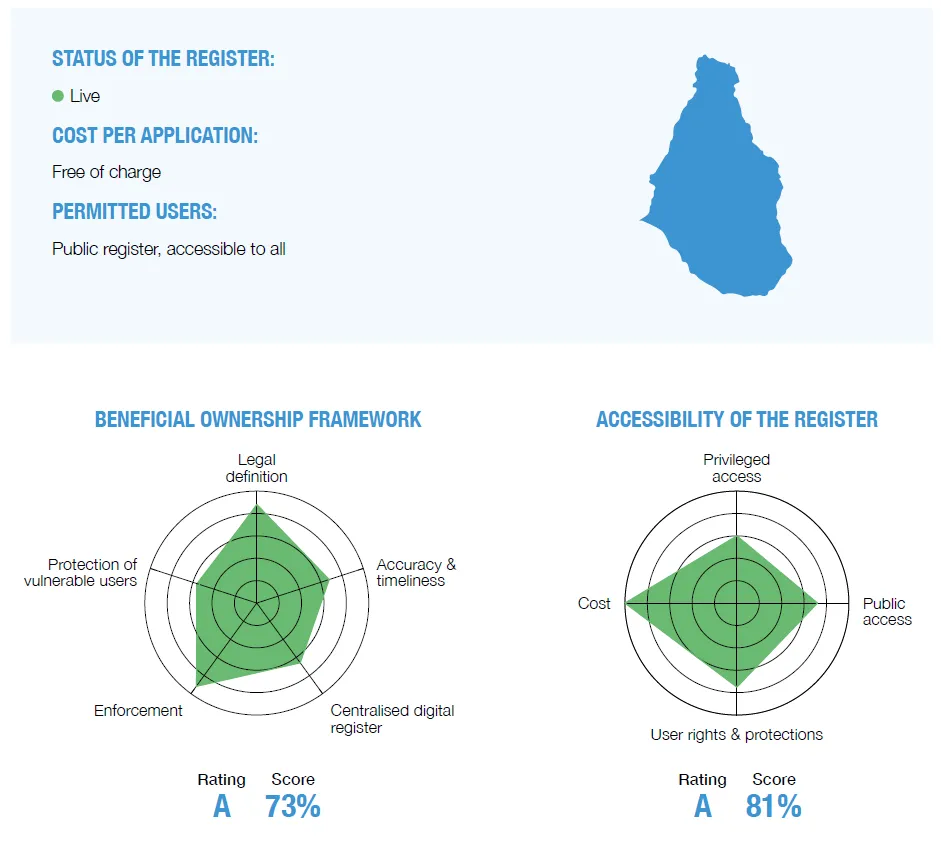

Montserrat

Background

Montserrat, also known as the ‘Emerald Isle of the Caribbean’, is home to less than 5,000 people.

In October 2024, Montserrat introduced a public register of beneficial ownership, which is open to all, and free of charge.

Risks and vulnerabilities

Key risks

Money laundering derived from sexual exploitation, fraud, human trafficking, migrant smuggling, and illicit trafficking in narcotic drugs and psychotropic substances

Vulnerabilities

Heightened risks of drug smuggling and human trafficking are linked to vulnerable borders and geographic proximity to Antigua & Barbuda, St. Kitts & Nevis, the Dominican Republic, and Haiti. Vulnerable sectors include banking, remittance, and real estate.

FATF status

In 2025, the FATF review found Montserrat to have increased its awareness and response to money laundering threats – but it recognised that Montserrat is not a major financial centre and risks are limited.

Key strengths

- Definition of beneficial owner almost fully aligns with international guidelines, with a strong similarity to the UK’s definition of ‘people with significant control’.

- Obligations to report beneficial ownership apply to companies and their owners, with potentially substantial financial penalties for non-compliance or false statements.

- Public register: Montserrat has established a public, centralised and online register which allows users to access details about beneficial owners and directors, and is expected to include filing history and other relevant documents in the near future. Basic shareholder information is also available to the public.

Protection of vulnerable individuals: Beneficial owners can only apply to withhold their information from disclosure in limited circumstances and must supply evidence to support their application.

Key weaknesses

- Scope of the register: Unlikely to disclose parties to trusts controlling companies, providing a crucial transparency loophole and undermining the effectiveness of the disclosure regime.

- Discrepancy reporting: There are no explicit requirements on competent authorities or regulated entities to report discrepancies they identify between their customer due diligence (or other data they hold) and the register.

Bulk download / API unavailable: Montserrat does not allow users to access the entirety of the data in machine-readable formats, as is the case with the UK’s Companies House register.

How Montserrat can deliver on its transparency commitments

Enable machine-readable, bulk access and advanced search of the register to facilitate research and analysis, enhancing the effectiveness of Montserrat’s register. Broaden the scope of the register to allow users to access information to parties of trusts controlling companies.

Methodology

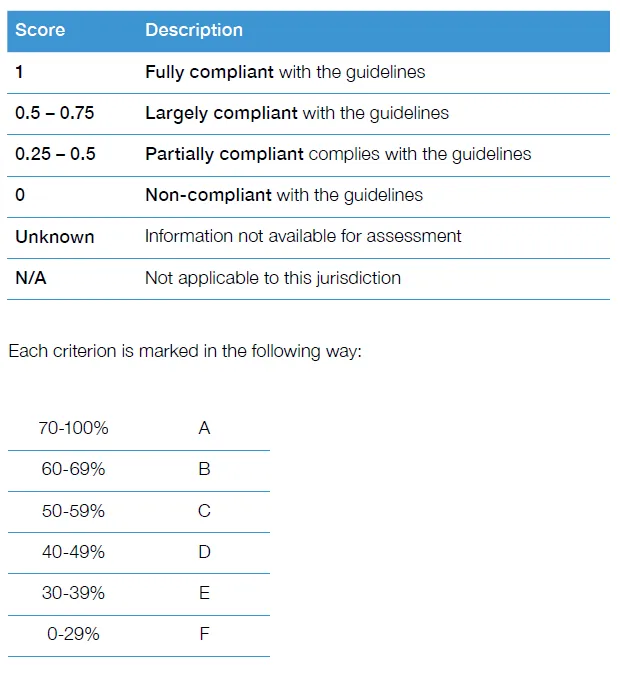

Our assessment is based on the rating of 92 criteria, set out in our blueprint published earlier this year. Each criterion has been marked between 0 and 1, based on our understanding and experience of the legal and policy frameworks introduced in Cayman, Bermuda, BVI and Montserrat. Where answers were not available in existing legislation, policy statements or other consultation document, we wrote to each jurisdiction, asking them to clarify.

Beneficial Ownership Framework

Legal definition assesses how beneficial owners are defined in law, including whether the definition covers all relevant legal entities, whether thresholds are appropriate, and whether any exemptions are narrowly tailored and justified.

Accuracy & timeliness examines the obligations placed on beneficial owners and legal entities to submit accurate information and to update it promptly when changes occur. Also looks at whether appropriate checks are performed to ensure data quality.

Centralised, digital data evaluates whether beneficial ownership information is held in a central register that is digital, machine-readable and searchable. This includes considerations such as unique identifiers, auditability of the data and overall usability.

Enforcement considers the availability and proportionality of both administrative and criminal sanctions for noncompliance. This includes sanctions for legal entities, directors, beneficial owners, and any third parties responsible for filings.

Protection of vulnerable users assesses whether the framework includes narrowly defined provisions to protect individuals who face a well-evidenced and exceptional risk of harm if their beneficial ownership information is disclosed. It also includes requirements around transparency.

Accessibility of the Register

Privileged access looks at the level of access granted to law enforcement agencies, competent authorities, and obliged entities (e.g., financial institutions) regulated for anti-money laundering.

Public access examines what information is available to the public and under what conditions. Criteria vary depending on whether the jurisdiction has committed to adopting a public access register or a legitimate interest register.

Modalities of access (legitimate interest models only) assesses how users can demonstrate legitimate interest, the clarity of the criteria, the efficiency of the process, and whether access is timely and not overly burdensome.

Cost evaluates whether access costs, if any, are reasonable and proportionate for different types of users, including for commercial and non-commercial use.

User rights & protections considers whether users are free to reuse and analyse the data they obtain and whether their identity is protected, particularly in systems where users must apply or register to access information.

Each criterion is marked in the following way:

Conclusion

When implemented effectively, corporate transparency is a vital tool in combating corruption and stemming the flow of illicit wealth. It enables investigators, journalists, and law enforcement agencies to scrutinise suspicious activity. Legitimate businesses also rely on transparency to identify the true owners of companies and their assets, ensuring they do not inadvertently facilitate transactions linked to theft, sanctions evasion, or other criminal activity.

Public access remains the most straightforward and cost-effective way of ensuring not only that the appropriate users can access beneficial ownership data, but that the data is of high quality. Public disclosure creates a natural deterrent and encourages self-policing. Widespread access to the data also enhances its reliability, as a broader range of users can identify and challenge inaccuracies or inconsistencies.

Where the registers are designed to serve a narrower purpose, legitimate interest models can still play a role in tackling money laundering and its predicate offences. However, these are significantly more complex and resource-intensive to establish. They require Overseas Territories to define broad, inclusive categories of users who can access, publish, and utilise the data without undue restrictions. Without this, such registers risk falling short of their stated objectives.

Unfortunately, Bermuda, the British Virgin Islands and Cayman Islands have clearly failed to meet the standards they agreed to meet during the 2024 Joint Ministerial Council – and are offering a piecemeal approach which does little to enhance transparency and scrutiny of beneficial ownership data.

The blueprint published over the summer provides clear guidance for Overseas Territories wishing to enhance their registers and meet the transparency commitments they made repeatedly to various UK governments. By adhering to these principles, jurisdictions can maximise the impact of their registers and play a meaningful role in the global fight against corruption.

As this UK Government prepares to host an international summit on illicit finance, meaningful access to beneficial ownership registers should not be optional. Without decisive action, illicit wealth will continue to flow through the UK’s backdoor, enabling organised crime groups and kleptocrats to conceal assets, evade sanctions, and undermine the UK economy. These standards should serve as a reference for setting parameters and expectations toward the Overseas Territories’ delivery.