Business Integrity

Read more

As the January 2025 deadline for first disclosures under the Corporate Sustainability Reporting Directive (CSRD) draws closer, Transparency International UK’s new report Preparing for the CSRD: ‘Corruption and Bribery’ and ‘Political Engagement’ examines the significance of this landmark EU legislation for corporate transparency.

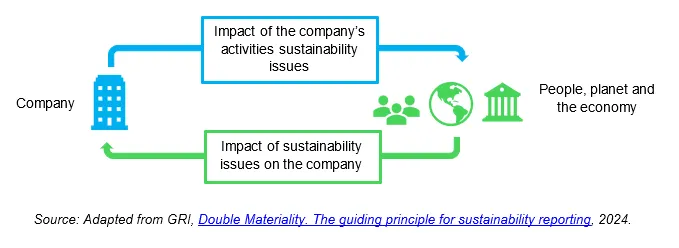

The CSRD requires companies in scope to publicly report information on their material sustainability impacts, risks and opportunities (identified by conducting a materiality assessment), including on ABC and political engagement. This reporting needs to be conducted in line with the accompanying European Sustainability Reporting Standards (ESRS). Our research outlines what companies can do in relation to anti-bribery and corruption (ABC) and political engagement when preparing for the CSRD.

Why is the CSRD significant for ABC?

The CSRD raises the bar on corporate sustainability reporting, with the ESRS containing around 85 disclosure requirements and over 1000 potential data points. This is important because it:

Yes! ABC and political engagement are core sustainability topics. Their incorporation reflects that corruption has a negative impact on companies’ financial bottom lines and can equally harm the societies and environments in which they operate. Corporate political engagement (both lobbying and political contributions) carries a risk of undue influence on policy making if not conducted responsibly and transparently.

Our research published in May 2023, with the International Federation of Accountants and World Economic Forum Partnering Against Corruption Initiative (PACI), shows that 95 per cent of global companies disclose some ABC information in their sustainability reports.

Our latest research finds that, of a sample of 90 UK listed companies, 35 per cent identify ABC and 23 per cent identify political engagement as material sustainability matters.

Companies which identify “corruption and bribery” and “political engagement” as material will need to report in line with ESRS G1 Business conduct. This could include reporting information on:

Our mapping document contains a full list of ABC and political engagement disclosure requirements in the ESRS and other key sustainability reporting standards. This mapping provides an overview of what companies may already be reporting and can be used to help boost corporate transparency on corruption-related matters.

There’s lots companies can be doing to prepare for the evolving sustainability reporting expectations (including for companies not directly subject to the CSRD):

The CSRD brings significant changes in how companies should evaluate and communicate sustainability information, including relating to ABC and political engagement. This is a positive step for corporate transparency and should enhance the utility of corporate disclosures. Now, the ball is in the court of companies to adapt and adjust to these new reporting and materiality assessment horizons.

Our Business Integrity Forum provides companies with the space to discuss how topics like CSRD are relevant to their ABC work. If you’d like to find out more about our corporate membership, contact [email protected]